How does getting a car insurance quote work?

A car insurance quote is an estimate of how much an insurance company will charge you for coverage. It is based on the information you provide about yourself, your car, and your driving history. It is not a guaranteed price; the final price you pay might be slightly different after a full application and underwriting process.

Each company uses a custom formula to calculate quotes, so checking quotes from multiple companies to find the lowest rate is a good idea. Once you submit a quote request, insurance companies assess your risk level. They review your information to determine the likelihood you would get into an accident and how much a claim would cost them.

What information is needed to get a car insurance quote?

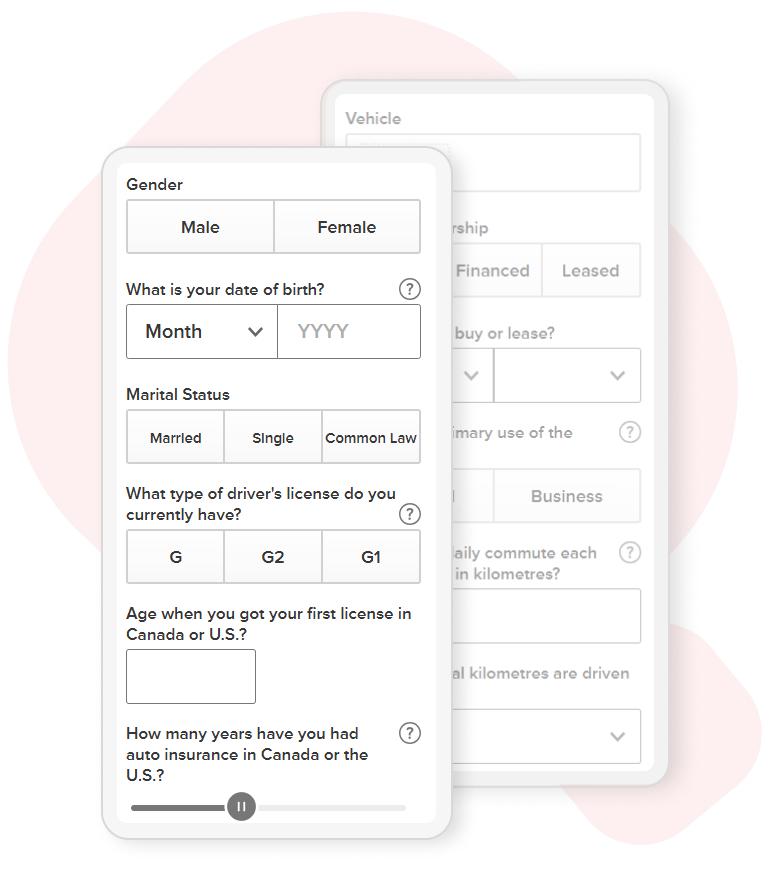

![image of information needed to get a car insurance quote]()

As part of the quoting process, you will answer a series of questions about yourself, your driving habits, and your vehicle. Here is the information you will need to get a car insurance quote:

- Basic personal information: your name, gender, age, phone number, and email.

- Mailing address and postal code: your level of risk is associated with where you live. Certain cities, neighbourhoods, and postal codes have more traffic, accidents, thefts, and expensive claims.

- Driver's licence: to show proof of your licence type and its validity.

- Vehicle make, model, and year: your vehicle type and value affect the cost of insuring it. A car that is a common target for theft will be more expensive to insure.

- Driving habits: how many kilometres you drive and whether you use your car for personal or business use.

- Insurance and driving history: a clean record is rewarded with cheaper insurance; a poor history increases premiums.

- Coverage requirements: the level of protection you choose affects your premium.

- Policy start date: tell your advisor when you need the policy to start.

Always be honest with the information you provide. False or misleading information makes your quote inaccurate and is grounds for a policy to be cancelled or a claim denied. Accurate information gets you a cheaper, reliable quote.

How long do car insurance quotes last?

It depends on the provider. For some insurers, quotes are valid for 30 or 60 days; some may be longer or shorter. Speak with your insurance advisor for clarification. If you receive a quote you like, act quickly to secure the rate, as premiums can change as often as quarterly.